Dear Stripe community,

Last year, businesses running on Stripe generated $1.9

trillion in total volume, up 34% from 2024, and

equivalent to roughly 1.6% of global GDP. Our

programmable financial services now power more than

5 million businesses directly or via platforms, including

all of the top AI companies, many of the largest bluechip companies (90% of the Dow Jones Industrial

Average), most of the biggest tech companies (80% of

the Nasdaq 100), and a significant fraction of freshly

minted startups (25% of all Delaware corporations are

now created with Stripe Atlas). Beyond payments,

these businesses are using Stripe to accelerate their

growth with billing and subscription management, tax

compliance, fraud prevention, embedded finance,

global treasury management, and much besides. Link,

the easiest way to pay online, is now used by more than

200 million people.

Stripe remained robustly profitable, allowing us to

continue investing heavily in product development

(with more than 350 product updates last year) as well

as acquisitions. Since our last update, we acquired

Privy, which powers more than 110 million

programmable wallets, and Metronome, which powers

the intricate usage-based billing models used by

companies like OpenAI, Anthropic, Confluent, and

NVIDIA. Metronome joins our Revenue suite, which is

on track to hit an annual run rate of $1 billion this year.

All in all, 2025 was a strong year for the internet

economy, and we’re delighted to see so many of

Stripe’s customers do so well

At heart, competitive markets are a sorting machine.

They direct profits, capital, and talent to the places of

greatest impact, as determined by customers voting

with their wallets. Historically, this sorting happened

methodically. It typically took decades for a household

name to be unseated or for a new entrant to reach

meaningful scale.

The sorting machine is now whirring faster: winners

and losers are being anointed more quickly and more

intensely. Today, the most profitable third of publicly

listed companies in the US account for two-thirds of

total market capitalization, the highest share since

data began in 1963. And much of this is a story of profit

concentration, not just valuations: the top 10% of the

S&P 500 by market cap now account for roughly 59%

of the index’s total profits, which is elevated relative to

recent history

The largest 50 companies account for 59% of profit

et income concentration in the S&P 5

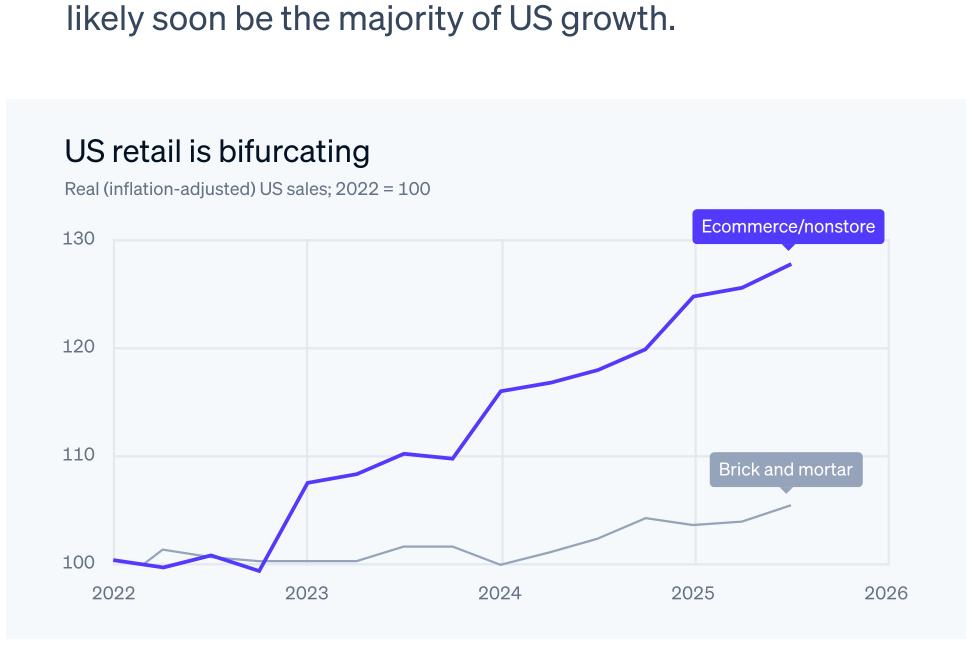

Much of this is driven by bifurcation within industries.

In retail, for example, US brick-and-mortar sales grew

just 5% over the past 3 years, whereas ecommerce

sales grew 30% over the same period (both in inflationadjusted terms). In air travel, the “big 3” of American,

Delta, and United all increased their share of industry

revenues and profits over the past decade. (Indeed,

Delta and United accounted for nearly all US airline

profits in 2025.) In healthcare, hospital and insurer

profit shares have contracted significantly since 2019,

but health tech is on track to exceed $110 billion in

EBITDA by 2029. Each sector has its own particular

dynamics, but the pattern is clear: a cohort of

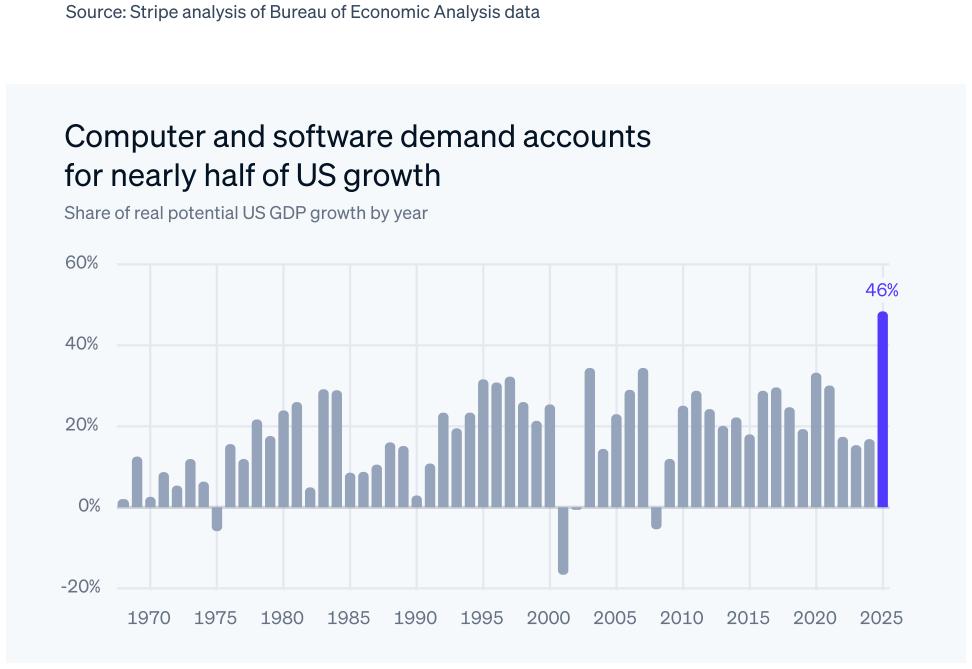

companies is pulling away. Economy-wide, demand for

software, computers, and data center investment

drove nearly half of all US GDP growth in 2025 and will

likely soon be the majority of US growth

US retail is bifurcatin

Real (inflation-adjusted) US sales

Source: Stripe analysis of Bureau of Economic Analysis dat

Computer and software demand accounts

for nearly half of US growt

Share of real potential US GDP growth by yea

Source: Bureau of Economic Analysis, Congressional Budget Office, Stripe analysi

Based on what we can tell from the set of businesses

that started on Stripe in 2025—a remarkable cohort—

there are no signs of the sorting machine slackening. In

2025, many more new companies joined Stripe than

ever before, with more than half of them (57%) based

outside the US. This new cohort is by far the highest

performing and fastest moving we’ve ever seen,

growing around 50% faster than the 2024 cohort. The

number of companies reaching $10 million ARR within

3 months of launch was double the 2024 count.

This seems to be part of a larger expansion and

acceleration in our industry. After years of relative

calm, the number of iOS apps released in December

2025 jumped by 60% year over year. (Someone should

check the App Store review team’s sleep scores.) Even

code production is accelerating: pushes to GitHub,

which grew roughly 10%–12% in prior years, surged 41%

between Q3 2024 and Q3 2025.

As building gets easier, we’re working on making Stripe

even simpler to integrate—including for the agents.

We recently introduced claimable sandboxes, which let

you start using Stripe directly from your AI coding tools

like Manus, Base44, Replit, and Vercel. When you’re

done with v1 and your product is ready to launch, that

sandbox converts into a live Stripe account with its

configuration intact. More than 100,000 sandboxes

have been created this way.

We’re also improving Stripe Atlas, the world’s easiest

way to incorporate a business, which saw a 41%

increase in company formations last year. Atlas

companies are monetizing sooner: in 2025, 20% of

Atlas startups charged their first customer within 30

days, up from 8% in 2020.

As we look at these figures, there is an obvious

question: is 2025 an anomaly or the beginning of a new

regime? Time will adjudicate, but our best guess is that

the 2025 acceleration is the start of a larger inflection

in entrepreneurship and creativity facilitated by

advances in large language models. We have an

ambitious roadmap of improvements planned. Stripe

will be the best way to build a business in the era of AI

For those with aspirations to “go global,” the

conventional playbook used to be a steady, sequential

progression: win at home, then push abroad. It took

Coca-Cola 20 years to bottle its first soda in Cuba,

while McDonald’s and Starbucks waited 27 and 16

years, respectively, to serve their first customers

in Canada.

After the arrival of the World Wide Web, free services

tended to launch globally, but their monetization

machinery still operated with a time delay. When

Facebook changed from a college-only network to a

public platform in 2006, anyone with a browser could

create an account, but anyone with money couldn’t

necessarily advertise. Support for international

currencies didn’t arrive until 2009, five years after the

company was founded. For its part, Google only

accepted its first GBP payment from an advertiser in

the UK (a live lobster mail order firm!) in 2002, four

years after launching its search product globally.

Over the last few years, the country-by-country

expansion model has melted away. The “domestic

market” for a new generation of internet businesses is

the internet itself. Nearly every AI product you’ve heard

of is all the rage in every country you’ve heard of.

ChatGPT, Claude, Replit, Lovable, Base44, Vercel,

Cursor, Midjourney, and many more launched globally

by default.

This isn’t merely about incremental revenue from a

“long tail” of international users. In many cases, the

“long tail” is much of the dog. Among Stripe

businesses with mostly international revenue, 30% of

that revenue comes from countries that are neither

their home market nor one of the top 10 global

economies.

This is possible largely due to infrastructure that no

longer makes foreign demand feel foreign. Last year,

we enabled businesses to launch a localized checkout

in more than 100 countries simultaneously, complete

with localized pricing to maximize conversion, more

than 120 payment methods, and local tax compliance

supported out of the box.

Sometimes improved infrastructure is only felt after

decades; other times, pent-up demand reveals itself

overnight. Gamma is a California-based AI platform

used by 70 million people to create presentations.

When Gamma joined the first cohort of businesses on

Stripe to accept UPI payments in India, its Indian

revenue leapt 22% that same month.

Ironically, the tech companies most constrained by

barriers of financial geography have tended to be

fintechs themselves. Twelve years after Chime

launched, you can only open a new Chime account

from inside the US. Nubank, founded in 2013, served

only Brazil for its first six years and added only two

other countries in the last six. Even at Stripe, our

Issuing product is available in only 22 countries some 7

years after launch—faster than most, but not as fast as

we would like.

This is also changing. The latest cohort of fintech

companies—Sling Money, DolarApp, Félix, and KAST,

to name a few—are building global financial apps right

out of the gate. Similarly, last year we launched our first

globally native product, Financial Accounts, which

businesses can use to hold, send, and receive funds.

We made it available to businesses in more than 100

countries on day one. The progress is in large part due

to stablecoins, whose borderlessness allows fintechs

to set up infrastructure that works everywhere. Globalby-default financial services are, for the first time, a real

possibility

It may be a crypto winter, but it’s a stablecoin summer.

After a decade of stablecoin volumes tracking the

undulations of crypto asset prices, last year saw a clear

divergence. In 2025, the price of Bitcoin dropped

precipitously (and is now down 50% from October), but

stablecoin payments volume doubled to around $400

billion, 60% of which is estimated to represent B2B

payments. Bridge, the stablecoin orchestration

platform we acquired, saw volume more than

quadruple. Stablecoin payments are advancing quietly

and inexorably as real-world uptake continues apace.

This growth has been catalyzed by a profusion of new

capabilities. A Y Combinator founder can now receive

funding in stablecoins, hold them in a Stripe financial

account, and use them to pay their first engineers, who

could be anywhere in the world. SaaS platforms are

using stablecoins to collect recurring payments,

thanks to a new smart contract that obviates the need

for wallet owners to manually sign each transaction.

Enterprises leaning on stablecoins to expand

internationally now have better tools to embed digital

wallets directly into their core products. With Privy,

companies like Ramp and Deel have a single API to

provision easy-to-use wallets in both custodial and

noncustodial models. This makes it possible to build

fully global products on day one.

The interoperability between crypto and fiat is also

rapidly improving. In April, Bridge partnered with Visa

to introduce cards that allow businesses and

consumers to spend their stablecoins just like any

other card. The payment is deducted from a stablecoin

balance and automatically converted to the local

currency; the business receives the funds just like any

other payment, serenely insulated from the underlying

stablecoin mechanics. Phantom, one of the most

popular crypto wallets with 20 million monthly active

users, is using Bridge to roll out stablecoin-backed

cards to its customers.

As we prepare for a world of massive stablecoin

adoption, we spent time last year thinking about

blockchains. Today’s blockchains have been designed

for trading and DeFi, and the attributes that matter for

payments (including throughput, reliability, cost

predictability, and privacy) have not been a significant

focus. Bitcoin processes fewer than 10 transactions per

second. Last year, a memecoin trading frenzy on one of

the major blockchains delayed payouts for one Bridge

user by over 12 hours and spiked per-transaction

prices 35×. While such operational issues are already

significant, they will only intensify, for we expect the

appetite for transactions to grow a great deal. In our

view, agents will most likely soon be responsible for

most internet transactions, and we will likely need

blockchains that support more than one million—or

even one billion—transactions per second.

In September, we unveiled Tempo, a blockchain

purpose-built for payments, incubated together with

Paradigm. With Tempo, businesses get dedicated

payment lanes, sub-second finality, opt-in privacy, and

interoperability with compliance and accounting

systems. These features may sound prosaic, but they

matter a great deal for infrastructure that supports

real-world economic activity. Companies like Visa,

Nubank, and Shopify are already testing Tempo for a

number of use cases, including global payouts,

embedded finance, and remittances. Klarna, whose

CEO was once a self-proclaimed crypto skeptic,

became the first bank to launch a stablecoin—

KlarnaUSD—on the Tempo testnet, using Bridge’s

Open Issuance to facilitate faster and cheaper crossborder settlement. Tempo’s architecture is also

particularly well suited to agentic payments and

microtransactions. Tempo’s mainnet will be launching

soon, and we look forward to seeing what ambitious

businesses decide to build with it

Since 2008, GDP per capita growth has been a

sluggish 1.0% in OECD countries—down from 2.8% a

year, on average, for the 46 prior years (when data

begins). It’s tempting to reach for local explanations

(Japan’s aging workforce, Brexit, Europe’s energy mix,

and so on), but there is good evidence that a significant

culprit is the sharp, global drop in the availability

of capital.

Sluggish 1.0% GDP growth in OECD countries since 200

Percentage chang

196 196 197 197 198 198 199 199 200 200 201 201 202 202

Indeed, in most OECD countries, capital requirements

for banks went up and capital access for small

businesses went down following the Global Financial

Crisis. Basel III reforms raised capital standards for

large banks around the world. In Ireland, bank lending

to small businesses dropped by more than 66%

between 2011 and 2019. In the UK, small business

lending contracted in 2012 and remained

weak thereafter.

The US fared slightly better, with easier access to

capital from nonbank lenders and 1.7% per capita GDP

growth over the last 15 years. But the broad trends,

post-Dodd-Frank, are the same: tightening of bank

rules and reduced access to capital for small

businesses. Since 2010, loans above $1 million are up

68%, while loans under $1 million are down 5%. Only

41% of small business loan applications were approved

in the US last year, down from 50% in 2015.

US business loans under $1M are down 5% since 201

Constant 2017$, Index: 2010 2 10

Source: Federal Deposit Insurance Corporation, Bureau of Economic Analysis, Stripe analysi

We created Stripe Capital to help solve the global

paucity of access to capital, especially for small

businesses. For businesses that use Stripe to accept

payments, their real-time revenue data makes for a

simple input to a lending decision. Businesses pay

back loans as a small percentage of their subsequent

sales, effectively drawing working capital forward from

their own growth. Funding volume grew 45% from

2024 to 2025, with Stripe Capital supporting more than

81,000 businesses. (Many of these businesses had

access to Stripe Capital funds directly through the

vertical SaaS platform on which they run—

GlossGenius for beauty salons, Tekmetric for auto

shops, Pixieset for photographers, and so on.)

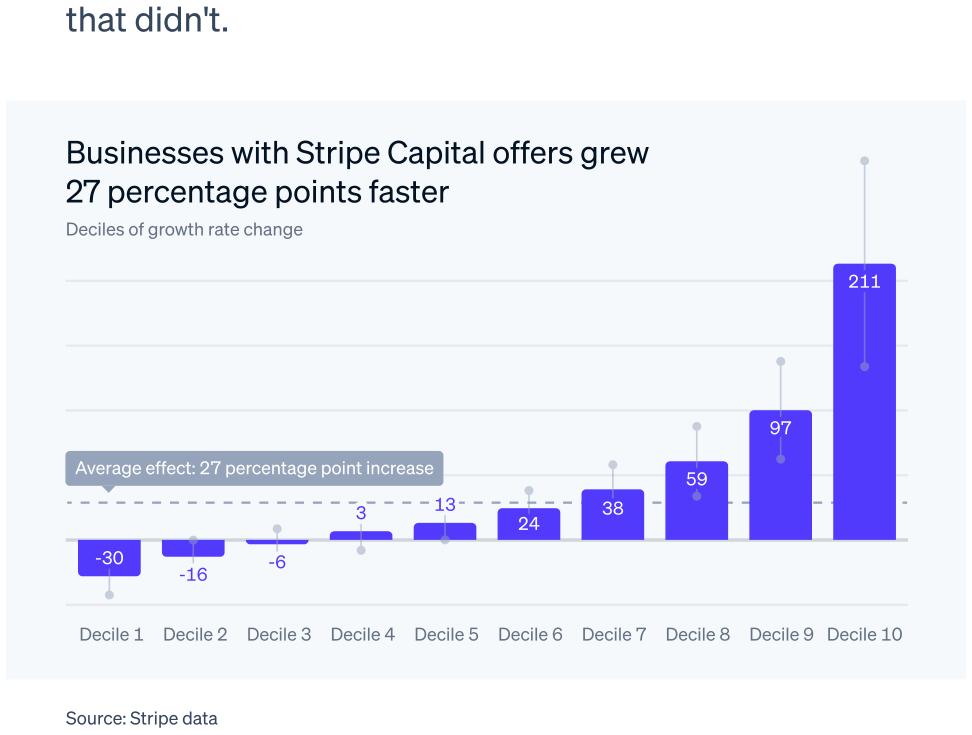

Over the last two years, we ran a randomized study to

understand the impact of Capital: when we help

businesses grease their wheels, how fast can they

grow? Turns out, a lot faster. Businesses that accepted

Capital offers grew 27 percentage points faster over

the following year than comparable businesses

that didn’t

Businesses with Stripe Capital offers grew

27 percentage points faste

Deciles of growth rate chang

Average effect: 27 percentage point increas

Decile Decile Decile Decile Decile Decile Decile Decile Decile Decile 1

The averages conceal a wide spread. The fastestgrowing decile of financed businesses grew more than

3× faster than comparable peers; the next decile grew

nearly 100 points faster. A representative example:

Xirsys, a server hosting business based in California,

used financing from Stripe Capital to set up additional

servers in China, India, and Japan, subsequently

doubling its revenue. Notably, even businesses with

low credit scores grew 11 to 18 percentage points faster

after receiving financing.

It’s speculative, but we wonder whether access to

capital will become a more important factor in

economic outcomes over the coming years, as

advances in artificial intelligence increase the returns

on investment

For mature businesses, there are notoriously few

guaranteed growth levers hiding in plain sight, and the

most enticing don’t always work out.

Take advertising. In 2019, Gillette won a Silver Lion at

Cannes for its ad, “The Best Men Can Be.” Later that

year, P&G took an $8 billion write-down on the

business, as the award-winning campaign failed to

ignite growth. More recently, a campaign for Indian

Railways won a Grand Prix and 6 Gold Lions at Cannes

in 2025 for its golden-ticket-style daily lottery (each

day, 1 train ticket number was eligible to win 10,000

rupees), but the campaign was shut down after 8

weeks with “no discernible increase in ticket sales.”

This is why, 15 years in, we remain so evangelically

animated about payments. Unlike more speculative

paths to growth, optimizing your payments setup is

almost guaranteed to yield extra revenue and to be

among the highest-ROI growth activities you

could undertake.

Microsoft, for example, evaluates the precise

performance of each of its payment service providers

on a monthly basis. Between June 1 and October 1,

Stripe delivered a meaningful increase in authorization

rates for Microsoft using a combination of Adaptive

Acceptance, card account updater, network tokens,

and more. As a result, Microsoft is now routing a larger

share of its payments through Stripe.

Gatwick Airport had been dealing with a string of failed

payments, disputes, and customer complaints under

its previous payment provider. After switching to

Stripe, payment acceptance rose by 2.5 percentage

points. Following an A/B test against its former

payment provider, FICO implemented Stripe and saw a

1 percentage point increase in authorization rates.

Telehealth company Ro saw a 2% increase in auth rates

and a 3% decrease in dispute activity over the last 12

months with Stripe, resulting in tens of millions of

dollars annually.

Most businesses are today operating in what we call

low revenue mode, running on unoptimized payments

infrastructure that’s leaking dollars left, right, and

center through conversion, auth, and fraud prevention

rates that should be so much better.

High revenue mode looks like a checkout that adapts

differently to each customer. You should be pricing

your products in local currency, and offering the right

set of the hundreds of local payment methods that are

most relevant. Presenting BLIK payments to your

customers in Poland drives an average 46% increase in

checkout conversion; offering Pix does the same for

customers in Brazil, with a 31% average conversion

uplift. This is all powered by a decade-long investment

in AI, including our Payments Foundation Model and

AI-powered services like Stripe Radar, Optimized

Checkout Suite, and Authorization Boost that quietly

optimize billions of dollars of transaction volume

every day.

Yet there’s still so much more room for improvement!

Last year, we began testing a new authentication

method that lets customers tap their card against their

phone. The tap validates the card’s NFC chip,

effectively proving the cardholder has the card in hand.

DoorDash, a partner in this trial, has seen meaningful

increases in conversion versus previous fraud checks,

while reducing chargeback rates. We also built new

models for Radar to handle a wider range of fraud

vectors emerging in response to the AI boom—in

particular, the very common attempts to steal AI

inference through abusing free trials or

similar mechanisms.

CEOs: splashy ad campaigns are good fun, but don’t

overlook the revenue growth right under your nose.

Your heads of payments almost surely deserve more

recognition. Let’s consider throwing them an awards

ceremony in the south of France for payments

optimizations. (Or for a foggier alternative, we’d love to

see them in San Francisco this April.

Much of the recent excitement in AI has been around

some form of tool use: models able to not only cogitate

on data in the pretraining corpus, but to go out and

search the web, use a browser, deploy code, or

similarly take action on the wider internet. The form of

tool use most relevant to our world is agentic

commerce: the idea that your AIs will soon be buying

stuff on your behalf.

Like much in AI, agentic commerce suffers from having

been overhyped too early in some corners. People

paint a utopian picture of autonomous agents planning

and executing all your commerce by knowing your

every whim. We find it helpful to build up to a broader

vision of agentic commerce in small chunks

Level 1: Eliminating web form

You research and decide what to buy. But filling out

web forms is no one’s favorite way to spend a few

minutes. It would be handy if you could simply send the

URL to your agent and have it fill out your payment and

shipping details, coming back to you with

the confirmation.

The system isn’t making any decisions for you. It’s just

typing and clicking “buy” on your behalf

Level 2: Descriptive searc

You stop searching for products or specific attributes

and start describing situations.

I need back-to-school supplies for a third grader in

Chicago, including clothes (nothing too itchy or

tight!), pencils, notebooks, and a lunch box. My

son likes KPop Demon Hunters and tennis. School

starts in late August

The system reasons across weather, materials, sizes,

durability, taste, reviews, and delivery timelines.

Specialized and long-tail products become easier to

find. Annoyingly blunt keyword search is no longer

a thing.

Level 3: Persistenc

You stop reintroducing yourself.

Find me options for back-to-school clothes for

Bobby

The system already knows your preferences and

remembers any requirements, inferred from your

previous conversations and purchases. You’re still

deciding what to buy, but you are choosing from a set

of options that already reflects your taste and budget.

Level 4: Delegatio

You stop choosing altogether.

Get the back-to-school shopping done. Keep it

under $400

The system handles the search, the evaluation

process, and the purchases on your behalf. You trust it

will weigh trade-offs as you would and choose things

your son will like. All you do is determine the budget.

(This is what most people mean today when they talk

about agentic commerce.

Level 5: Anticipatio

There is no prompt.

The system already knows the school calendar, your

son’s preferences, and your typical budget. All you do

is receive a notification: here’s the back-to-school list of

everything that’s been purchased. This is the most

futuristic vision, where the things you need show up

right before you need them, without you having to ask.

Today, the industry is hovering on the edge of levels

1 and 2.

We’re reminded of those few years in the mid-90s

when the structure of the internet we use today was

hashed out. Netscape developed graphical web

browsers. HTTP and HTML became the shared

application layer. URLs and DNS gained prominence.

At the time, no one knew exactly which protocols or

players would win out. There was an AltaVista for every

Google.

We’re in a similarly rare moment now with agentic

commerce, which has the potential to be

generationally impactful. As with the early internet, the

future success of agentic commerce is contingent on

universal interoperability. Our ascent through the five

levels depends on our ability to work together.

To that end, we’ve been busy! A few highlights from the

last year include:

With OpenAI, we developed the Agentic Commerce

Protocol (ACP) to establish a shared technical

language between AI platforms and businesses. It’s

open by design, working across payment providers

and AI platforms.

We introduced Shared Payment Tokens, a new

payment primitive that lets agents initiate

payments without exposing credentials. Even

businesses that don’t process payments with Stripe

can forward these tokens to their own vaults or

other processors as secure credentials.

We launched an Agentic Commerce Suite, which

provides tooling for businesses to sell across

multiple AI interfaces and protocols (including ACP

and, soon, the Universal Commerce Protocol that

Google unveiled last month) with a single

integration. Checkout, payments, and fraud

protection continue to work predictably

underneath. Brands already onboarding to our

Agentic Commerce Suite include Anthropologie,

Urban Outfitters, Etsy, Coach, and Kate Spade.

We launched machine payments, a way for

developers to charge agents directly for API calls,

MCP usage, and HTTP requests using stablecoin

micropayments. (Autonomous agents, themselves,

are emerging as a new customer type for internet

businesses to sell to.)

We partnered with OpenAI to power the first

shopping experiences inside ChatGPT. We are also

collaborating with Microsoft to bring similar

capabilities to Copilot.

There’s no forecasting exactly where agentic

commerce will be by the end of 2026, but it’s clear

we’ve already moved well beyond pure hype into a

phase of building and real-world experimentation. The

pace of change will likely only accelerate from here.

If all goes well, the little critters won’t be cooped up in

walled gardens, but will be zooming down the wideopen protocol highways.

Today’s entrepreneurs and innovators have tools and

reach that prior generations of industrialists could not

have fathomed. We will hopefully soon witness the

combinatorial effect of human ingenuity paying out in

the form of productivity gains and improved living

standards everywhere.

Last year, Joel Mokyr was awarded the Nobel Prize in

Economic Sciences. Mokyr is widely known for

emphasizing the importance of culture relative to the

traditional economic inputs of capital, labor, and

technology. Eighteenth-century industrialists didn’t

just have coal or geography on their side. They had a

new culture—an “improvement mindset” that saw the

status quo as imperfect and correctable.

In The Political Economy of Technological Change,

Mokyr also observed that new technologies have in the

past often failed, despite their economic superiority,

because technological decision-making implicates not

only suppliers and customers, but also a broad variety

of nonmarket “aggregators” (regulators, committees,

courts) that influence what is adopted.

As AI and the internet expand the scope of what’s

possible, synthetic impediments to adoption and

adaptation will become increasingly costly. Our

bifurcating economy shows that growth is contingent

on the application of useful knowledge and not some

preordained result of its abstract availability.

AI harbors the promise of enormously improving drug

discovery… but the potential will only be realized if we

make the regulatory process, including clinical trials,

faster and cheaper. Entrepreneurs in Europe can boost

tepid economies with new tools… but only if wellintentioned yet counterproductive burdens such as the

EU AI Act are curtailed. Next-generation approaches to

nuclear energy could usher in energy abundance… but

only if we overhaul vetocratic regulatory regimes.

Autonomous transport and logistics—from long-haul

trucking to drones—could dramatically reduce the

cost of physical goods… provided we don’t let a slurry

of local ordinances harden into a blockade.

Mokyr wrote about the importance of the Republic of

Letters in catalyzing the industrial revolution. Today, we

inhabit a Republic of Permissions: a filtering sieve of

nonmarket aggregators. While many of our strictures

are sensibly motivated, it’s more important than ever to

ensure that they carefully balance the benefits

achieved with the possibilities foreclosed.

We’re privileged to support many businesses with the

tenacity to show what’s possible. Mistral AI and

Bending Spoons are proving that world-class

European talent can puncture the regulatory

permafrost; Zipline and Varda are earning permissions

for intricate new hardware inch by inch; while Spring

Health and Maven Clinic are stitching together a new

software layer for modern healthcare.

We continue to believe both in the importance of ideas

in fueling economic progress and that many of the best

ideas are undervalued. The Stripe Press catalog is

home to many of the people, stories, and models we

think can contribute to the next set of improvements.

The team recently celebrated one million books sold.

Works in Progress, our magazine of underrated ideas

to improve the world, has also recently branched out

into print subscriptions. (Get yours over at

worksinprogress.co/print. We highly recommend it.

Much of this letter has been dedicated to advances in

AI, which can sometimes seem hard to keep up with.

The qualitative difference between just-released

products and last year’s state of the art is stark.

We’re reminded of the phenomenon of falling into a

large black hole. If you ever experience that particular

misfortune, you won’t actually feel anything special at

the moment you cross the event horizon: the path is

locally smooth, even though the space of possible

futures changes irrevocably upon crossing the

threshold.

We write this letter at what may well turn out to be the

advent of a different and hopefully much more

beneficent singularity. While much around us in 2026

feels similar to prior years, it is also clear that the next

decade will look very different to those just gone by.

We are as enthusiastic as ever about how vibrant

entrepreneurship and wise cultures can contribute to

more successful future societies, and we hope that

Stripe can play a small role. And if you’re propelling

economic growth yourself—whether as an

entrepreneur, business leader, or financial

infrastructure builder—we hope to welcome you to

Stripe Sessions in April. As always, there’s much to

discuss.