Growth is getting hard from intensive competition, consolidation, and saturation

The end of the cycle

One of the best essays written last year was Elad Gil’s End of Cycle? – referencing our most recent 2007-2017 run on mobile and web software, and the implications for investing, startups, and entrepreneurs. Although he doesn’t directly talk about it, the end of a tech cycle has major implications for launching new products, growing existing product categories, because of a simple thing:

It gets much, much harder to grow new products or pivot existing ones into new markets

The reason for the above is that there are multiple trends – happening right now – that impede growth for new products. These trends are being driven by the biggest players – Google/Facebook, et al – but also by the significant leveling up around of practitioners in design/PM/data/growth.

We’ll look at a couple trends in this essay, including the following:

- Mobile platform consolidation

- Competition on paid channels

- Banner blindness = shitty clickthroughs

- Superior tooling

- Smarter, faster competitors

- Competing with boredom is easier than competing with Google/Facebook

These trends are powerful and critical to understanding why all of a sudden, entrepreneurs/investors are starting to get into many new fields (genomics, VTOL cars, cryptocurrency, autonomy, IoT, etc) in order to find new opportunities. After all, if you can’t grow in the existing markets, you very quickly need to get into new ones, as Elad describes:

One sign that technology markets often exhibit at the tail end of a cycle is a fast diversification of the types of startups getting funded. For example, following the core internet boom of the late 90s (Google, Yahoo!, eBay, PayPal), in early 2000 and 2001 there was a sudden diversification and investment into P2P and mobile (before mobile was ready) and then in 2002-2003 people started looking at CleanTech, Nanotech etc – industries that obviously all eventually failed from an entrepreneurial and investment return perspective.

Nanotech, cleantech, etc was the last cycle, and now we’re talking about the next one.

#1 Mobile platform consolidation

The new Google/Apple app duopoly is more concentrated, more closed, and far less rich (from a growth standpoint) as compared to web – which means that mobile is far more stagnant and harder to break into. App Store functionality like top ranking charts, “Essential” bundles of apps, editorialized “Featured App” sections, all help drive a winner-takes-all mobile ecosystem.

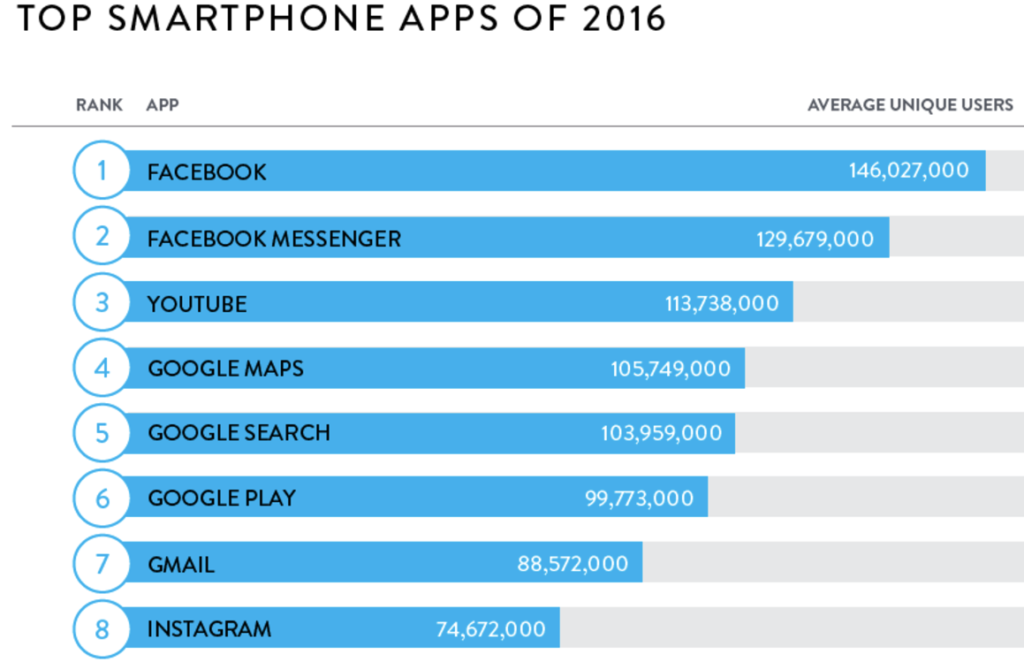

No wonder app store rankings have ossified over the years. Facebook and Google now control most of the Top 10 apps in the mobile ecosystem:

Source: Nielsen, Dec 2016

If you’re introducing a new app – whether unbundling a more complex app or launching a new startup – how do you break into this? There’s not a ton of organic opportunities. And the paid acquisition channels are getting saturated too.

#2 Competition on paid channels

Paying for acquisition is one of the key channels still available, if you can find the right untapped audience segments with high ROIs. This only works when prices aren’t bidded up and you don’t face too much competition for the same ad inventory. Unfortunately that’s not what’s happening.

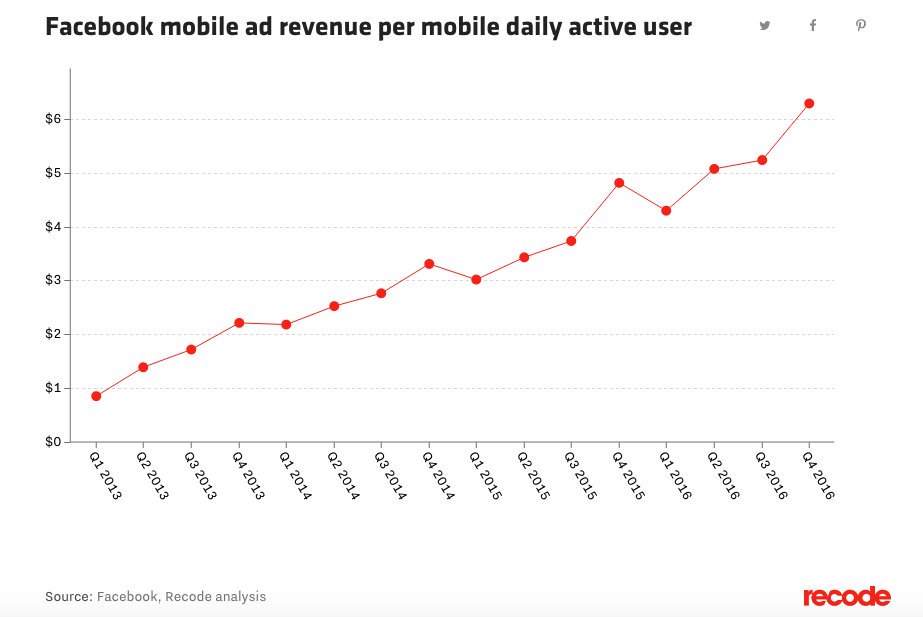

For example, let’s look at some of the dynamics of Facebook increasing their revenue per DAU over the last few years:

This is driven by a number of factors, of course – relevance, targeting, ad unit engagement, etc. – but it’s also because competition is getting fiercer on Facebook ads, not less, which is evidenced by the rapid increase in the advertiser count as well as the increase in revenue per user. In 2017, Facebook counts over 5 million advertisers on its platform, up from 4 million in Q3 of last year and 2 million in 2015. During its Q1 2017 earnings call, Facebook told investors that it expected ad revenue was approaching a saturation point, despite major growth in Q1 2017 earnings as compared to 2016. It’s currently at 2 billion users, with 17% YoY user growth, and its ability to add more inventory depends increasing its user base, or increasing users’ time spent on Facebook.

#3 Banner blindness = shitty clickthroughs

Additionally, everyone’s getting smarter about growth, including consumers. Today, most invite systems no longer have the same novelty value or efficacy as they did 10 years ago (Dropbox’ give/get was novel when it launched), and consumers’ “banner blindness” extends far beyond actual display advertising to encompass referral systems and virality programs.

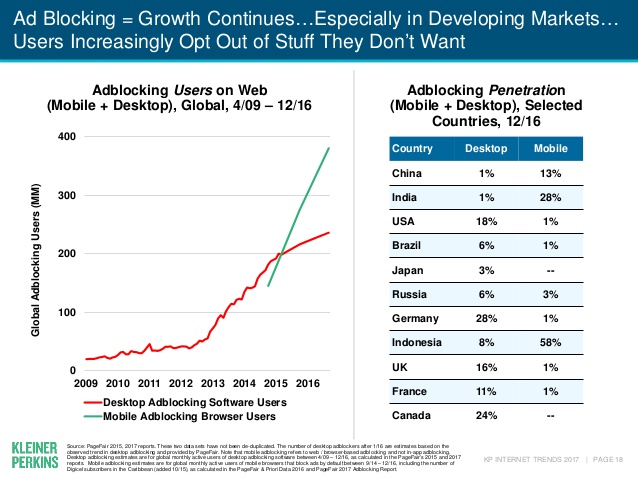

In Mary Meeker’s latest internet trends report, she reports that up to 1/3 of some countries are using ad blocking, and we’re quickly on our way to 600M internet MAU who can’t be reached by ads:

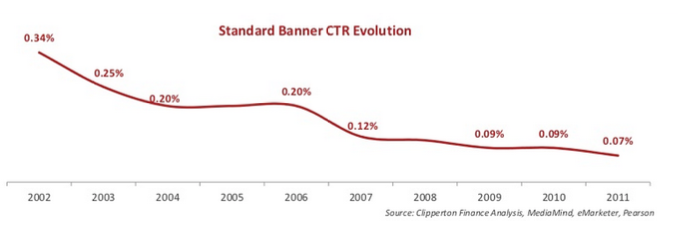

This is just the 2017 version of The Law of Shitty Clickthroughs, which I wrote about a few years ago, where I showed some stats indicating that email marketing open rates are on the decline:

… and that traditional banner CTRs seem to be asymptotically approaching zero:

These trends are troubling, and mean that these channels are getting less engagement per user, and we haven’t found amazing new channels to replace them.

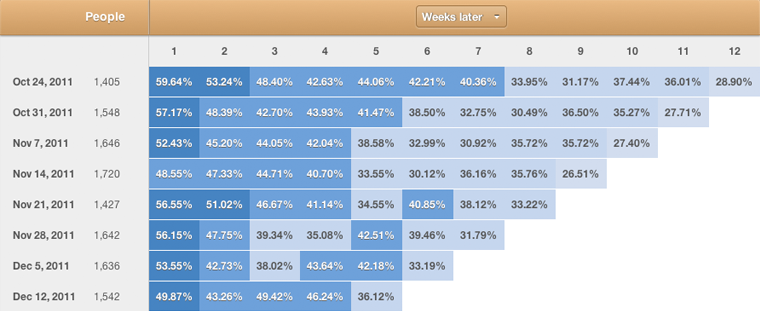

#4 Superior tooling – which levels the playing field

At the same time as advertising is getting more crowded, there’s also increasingly widespread availability and adoption of tools like Mixpanel, Leanplum, Optimizely and others that close the gap on being data-driven at companies.

Ten years ago, we used to look at total registered users. Cohort analysis was a sophisticated approach, and we also didn’t have a sense for MAU, DAU or other more granular metrics. One of the killer features of Mixpanel is that it made understanding cohort-based retention turnkey. It used to take a real investment of engineers, data scientists, and know how to be able to create simple graphs like this:

Now, it’s pretty much turnkey. You can get this chart from Mixpanel (and may others!) practically for free, as soon as you implement your analytics tracking.

In B2B, we’re seeing the same phenomenon. Outbound used to be painstaking and manual. Today, there are many sales tools that make outbound more accessible (Mixmax, Outreach, insidesales.com etc), which automates part of the process but also generates more noise and competition. Tasks that used to be more manual and higher friction are automated and easier, which leads to more people jumping in.

The result is that it makes everyone better. You and all your competitors understand your/their acquisition and retention bottlenecks. Everyone has an equal, data-driven shot at improving LTV, and as a corollary can spend more on ads.

#5 Smarter and faster competitors

It used to be that startups could count on their competitors to be big, dumb, and slow. Not anymore. We’ve all gotten smarter and faster, and that includes your competitors. It used to be that you could wait a few years before competitors would respond. Now the Facebooks, Hubspots and Salesforces of the world can and will copy you right away.

Most famously, we’ve seen Facebook fast follow Snap within their Messenger, Instagram, Whatsapp and core product:

But it’s not just consumer where this is happening:

- Dropbox <> Google Drive

- Slack <> Microsoft Teams

- YesWare <> Hubspot Sales

… and many more examples too.

#6 Competing with boredom is easier than competing with Facebook + Google

When the App Store first launched, competition was easy: Boredom. Mobile app developers were taking time away from easy, ‘idle’ activities like waiting in line, commuting etc. But today, acquiring a new app user means stealing a user’s time from their favorite existing app.

As we’re near the end of the cycle, companies have moved from non-zero sum to a zero-sum competition.

Instead of competing with boredom, we’re now competing with Silicon Valley’s top tech companies, who already have all your users (back to number 2 above). This also applies to the consumerized workplace, where new entrants will be competing to steal users’ time from Slack, Dropbox and other favorite apps. This is much, much harder because the incumbents have pretty great products! And proven distribution models to respond if needed.

How the industry is evolving, in response

The above trends are troubling for new products, and especially for startups. All 6 of these trends are scary, and they’ve emerged because we’re at the end of a cycle. There’s a variety of natural monopolistic trends (like app stores, ad platforms, etc), where everything with related to growth and traction is getting harder.

If companies want to stay in the mobile/software product categories, they need to evolve their strategies. I’ll save a deeper discussion for a future essay, but here are some observations on what’s happening:

- More money diverted to paid acquisition

- Deeper monetization to open up channels – especially paid

- Creation of paid referral programs to complement ad buying

- Personalization features that rely on lots of data to amp up targeting

- Products trying to deepen differentiation by solving hard(er) problems/tech

There seems to be a deepening in both monetization, differentiation, and personalization to help open up growth. This happens by solving more fundamental customer problems – especially those that help generate real $ value for people – but also helps open up paid channels, whether that’s advertising, referrals, or promos.

More discussion on this in a future writeup!

PS. Get new updates/analysis on tech and startups

I write a high-quality, weekly newsletter covering what’s happening in Silicon Valley, focused on startups, marketing, and mobile.